Fraud Prevention Ecommerce: UK Guide 2026

- fraud prevention ecommerce

- shopify fraud protection

- chargeback prevention

- ecommerce security

- uk ecommerce

Launched

July, 2026

UK online payment fraud losses were estimated at £4.4 billion in 2024, while UK merchants spend an average of 11% of revenue on fraud protection and absorb roughly £3.2 billion a year in fraudulent chargebacks according to Statista's UK e-commerce fraud overview. That should change how you think about fraud prevention ecommerce.

This isn't a narrow payments problem. It sits inside margin, operations, customer service, checkout performance, and retention. A store can lose money in two directions at once: by approving bad orders and by blocking good customers.

For a new Shopify Plus merchant, the job isn't to build the strictest fraud stack possible. It's to build a system that catches obvious abuse, escalates uncertain orders, and protects conversion where the customer is genuine. In the UK, that also means designing around Strong Customer Authentication (SCA) rather than treating regulation as an afterthought.

The High Stakes of Ecommerce Fraud in the UK

A single weak fraud rule can erase margin faster than many new Shopify Plus merchants expect. The loss rarely stops at one bad order. It spreads into fulfilment costs, support time, dispute work, payment acceptance, and customer trust.

That is the part merchants often underweight.

Fraud costs more than the stolen order

The obvious hit is straightforward. Goods go out, the payment fails later, and the chargeback follows. The harder part is what sits around that order and keeps costing money after the transaction has gone.

- Operational drag: Orders flagged for review pull staff away from merchandising, fulfilment, and customer service.

- False declines: A genuine customer gets blocked, gives up, and may not come back.

- Processor scrutiny: Rising dispute rates can lead to stricter monitoring, reserves, or tougher terms from payment partners.

- Support burden: Customers whose payments fail or accounts are misused expect fast answers, and your team has to provide them.

- Security spillover: Staff phishing and account compromise can feed payment fraud, which is why merchant teams also need basic controls around avoiding phishing attacks.

For UK merchants, there is another trade-off to manage. Strong Customer Authentication helps reduce some unauthorised card use, but poor setup can add checkout friction in the wrong places. The goal is not maximum challenge rates. The goal is to push high-risk transactions into stronger checks while letting low-risk genuine customers complete payment with as little interruption as possible.

Why fast-growing stores feel this first

Growth creates more exceptions. A store adds new shipping destinations, launches higher-ticket products, runs larger promotions, or sees a sudden surge from paid social. Each change gives fraudsters more room to test what your controls will tolerate.

I see this most often after a merchant scales faster than their processes. The checkout is working, orders are flowing, and fraud review still sits with a small team using inconsistent rules. That is when two expensive mistakes show up together. Bad orders get approved because nobody has time to investigate them properly, and good orders get cancelled because the team starts playing safe.

That is why fraud prevention ecommerce needs a balanced strategy, not a stack of tools switched on at full sensitivity. Protecting revenue means reducing fraud losses and reducing false positives at the same time. For UK merchants, it also means configuring SCA, payment rules, and manual review thresholds so they work together instead of fighting conversion.

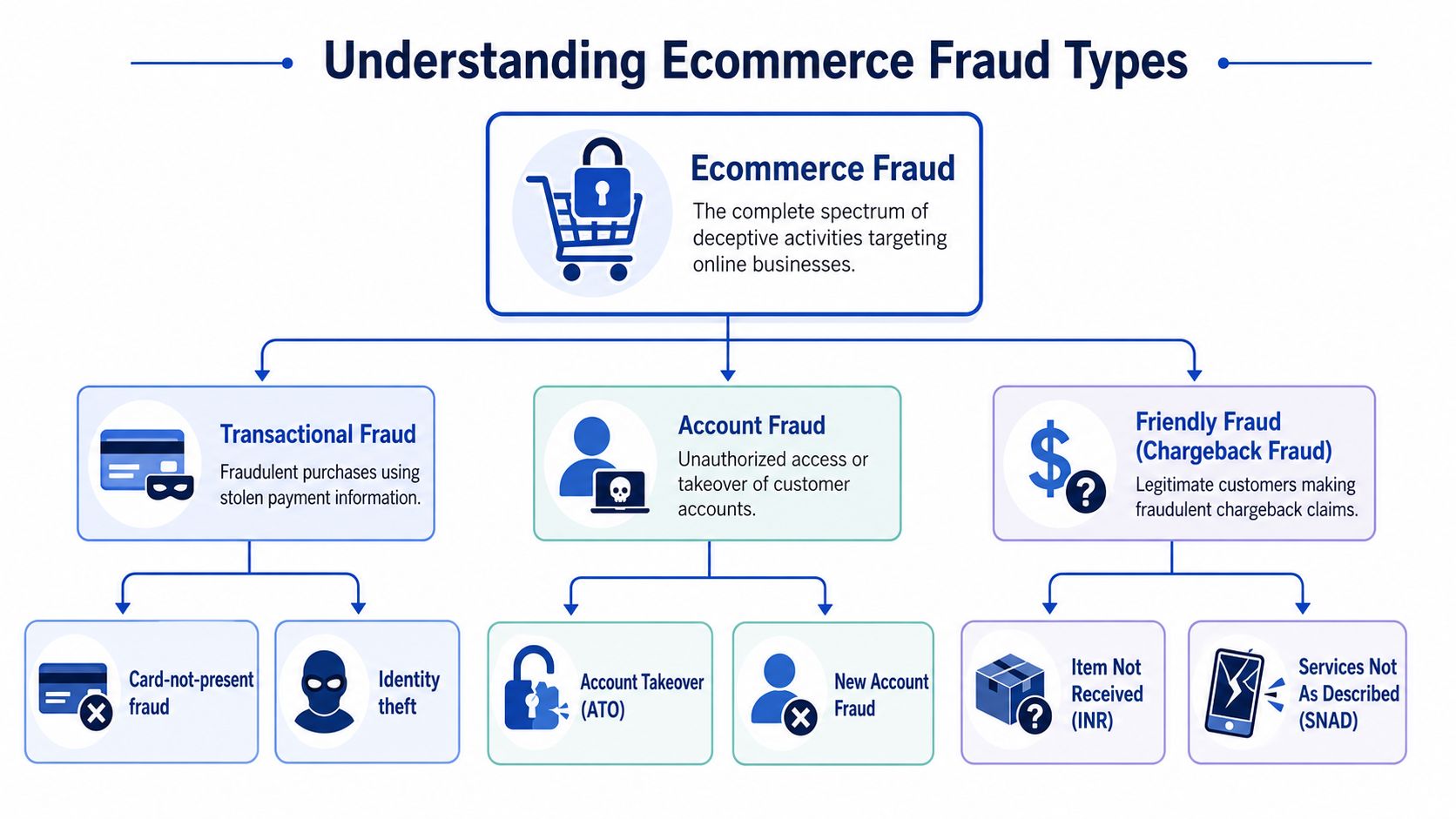

Understanding the Main Types of Ecommerce Fraud

Fraud isn't one thing. It helps to sort it by motive. Some attackers are outsiders using stolen payment details. Others are real customers abusing refunds or disputes. Others break into legitimate customer accounts and place orders that look normal on the surface.

Transactional fraud

This is the classic stolen-card scenario. The fraudster uses payment details they shouldn't have and tries to convert them into goods before the transaction is challenged.

Common patterns include:

- Card-not-present misuse: An order passes through online because there's no physical card inspection.

- Identity mismatch: Names, addresses, emails, and shipping choices don't fit together cleanly.

- Testing behaviour: A burst of attempted transactions can signal someone probing whether payment details work.

These orders often look rushed. Expedited shipping, unusual product mixes, or multiple attempts from the same session are typical warning signs.

Account fraud

This starts with access, not payment. A fraudster gets into a customer account, then uses stored cards, saved addresses, loyalty value, or account trust history to make the order appear legitimate.

That can include:

- Account takeover: A known customer account suddenly behaves differently.

- New account abuse: Fresh accounts appear and place risky orders straight away.

- Address switching: Shipping details change late in the flow or shortly after purchase.

If your team is also educating staff and customers on avoiding phishing attacks, you'll cut off one of the most common routes into account compromise.

Fraudsters don't care whether they beat your payment controls or your customer login. They'll use whichever path has less resistance.

Friendly fraud and chargeback abuse

This category is awkward because the customer may be real, the delivery may be real, and the payment may have been authorised correctly. The dispute arrives later.

A buyer might claim they didn't receive the item, didn't recognise the charge, or weren't satisfied with what was delivered. Sometimes that's a genuine service issue. Sometimes it's opportunistic abuse.

For merchants, this kind of fraud is costly because the order can look perfectly healthy at the point of purchase. That's why prevention doesn't end at checkout. Fulfilment records, communication quality, returns handling, and dispute evidence all matter.

Your First Line of Defence Payment Controls

Before you buy advanced software, tighten the controls inside the payment flow itself. These are the equivalent of locks on the front door. They won't stop every threat, but they remove a large amount of avoidable risk.

AVS and CVV still matter

For card payments, two checks remain basic hygiene:

- AVS checks: Compare the billing address details submitted at checkout with what the card issuer has on file.

- CVV checks: Confirm the customer has the card security code during payment.

Neither is perfect on its own. A fraudster can sometimes have enough stolen information to pass one or both. But when these checks are configured sensibly in your gateway, they give your fraud tools more context and reduce obvious low-quality attempts.

Don't make the mistake of treating these signals as absolute. An AVS mismatch doesn't always mean fraud. A legitimate customer can mistype a postcode, use an old billing address, or buy while travelling. Use the result as a risk input, not a blind rejection trigger.

SCA is the UK baseline

For UK merchants, Strong Customer Authentication is the foundation. Under PSD2 rules retained in UK law, SCA requires customers to authenticate ecommerce payments using two independent methods of verification. According to Riskified's summary of ecommerce fraud and SCA, the UK's mandatory adoption of SCA reduced unauthorised transaction fraud by an estimated 15% to 20% in its first year, and nearly 99% of UK online transactions now comply with SCA. The same source notes a 30% increase in consumer trust in digital payments.

That matters operationally because SCA changes how you design your checkout and your fraud rules. If your store fights SCA, your customers feel friction without clarity. If your store uses it well, you gain a strong default layer against unauthorised payment abuse.

What works in practice

A sensible payment-control setup usually looks like this:

- Enable gateway-level checks first: Turn on AVS, CVV, and the fraud settings provided by your payment processor.

- Map outcomes to actions: Approve low-risk orders, queue unclear ones, and decline the obvious failures.

- Use SCA as a targeted challenge: Let the strongest verification appear where risk justifies it.

- Review payment page security: Merchants dealing with card data or payment-page risks should understand DSS 4.0 compliance and reporting, especially around how payment environments are assessed.

- Keep PCI scope visible: If your checkout stack or integrations are changing, this guide to PCI compliance requirements is a useful operational reference.

Working principle: Put hard controls at the payment layer first. Everything else should refine decisions, not compensate for a weak checkout foundation.

Advanced Fraud Detection Techniques

Once the payment layer is secure, the next job is decision quality: merchants move from basic checks to systems that interpret behaviour, context, and patterns across orders.

Rules engines

Rules are the simplest place to start. They work like a security guard with a checklist.

You define conditions such as:

- high-risk combinations of billing and shipping data

- suspicious order patterns

- repeat attempts from the same device or session

- product categories that need review

Rules are useful because they're easy to understand and quick to change. If a specific abuse pattern appears, the fraud team can react the same day.

Their weakness is rigidity. Static rules don't adapt well when legitimate customer behaviour changes. They also tend to pile up. After enough exceptions, the logic becomes messy and hard to maintain.

Machine learning and behavioural analysis

Machine learning tools look for combinations that a simple rule set would miss. They're better at spotting subtle risk patterns across many signals, especially in larger stores with enough transaction history.

Behavioural analysis adds another layer. Instead of focusing only on order fields, it looks at how the customer interacts with the site. The shape of the session matters. Was the journey calm and consistent, or did it behave like an automated attempt or a rushed abuse pattern?

Modern fraud prevention ecommerce tends to outperform old manual-only setups. It doesn't rely on one red flag. It weighs context.

The best systems don't ask, “Did one field fail?” They ask, “Does this whole order behave like a real customer?”

Velocity checks and device fingerprinting in a UK SCA environment

Many UK merchants encounter a specific difficulty. Velocity checks help detect rapid fraud bursts, and device fingerprinting helps identify suspicious devices or repeated access patterns. Both are useful. The challenge is applying them without creating unnecessary friction or clashing with SCA workflows.

Ping Identity's guidance on ecommerce fraud detection highlights that UK merchants often lack practical direction on reconciling these tools with SCA's step-up validation methods. In practice, the cleanest approach is to use velocity and device signals as triggers for escalation, not as automatic rejection tools in every case.

A practical setup looks like this:

- Low risk: Let the order proceed with standard controls.

- Unclear risk: Trigger additional review or stronger authentication where your payment flow supports it.

- High confidence fraud: Block or cancel before fulfilment.

Comparing Fraud Detection Methods

| Method | How it Works | Best For | Weakness |

|---|---|---|---|

| Rule-based checks | Uses fixed conditions set by the merchant or fraud team | New stores, simple risk patterns, fast policy changes | Becomes blunt and over-restrictive if overused |

| Machine learning models | Learns from transaction history and changing patterns | Higher-volume stores with varied order behaviour | Needs oversight and clean operational feedback loops |

| Behavioural analysis | Evaluates session behaviour and customer interaction signals | Detecting subtle anomalies and non-obvious fraud | Harder to interpret without strong tooling |

| Velocity checks | Flags rapid repeat activity across orders or attempts | Card testing, burst attacks, promo abuse | Can catch genuine busy shoppers during promotions |

| Device fingerprinting | Tracks device-level consistency and reuse patterns | Repeat abuse, account risk, linked fraud activity | Should inform scoring, not replace broader review |

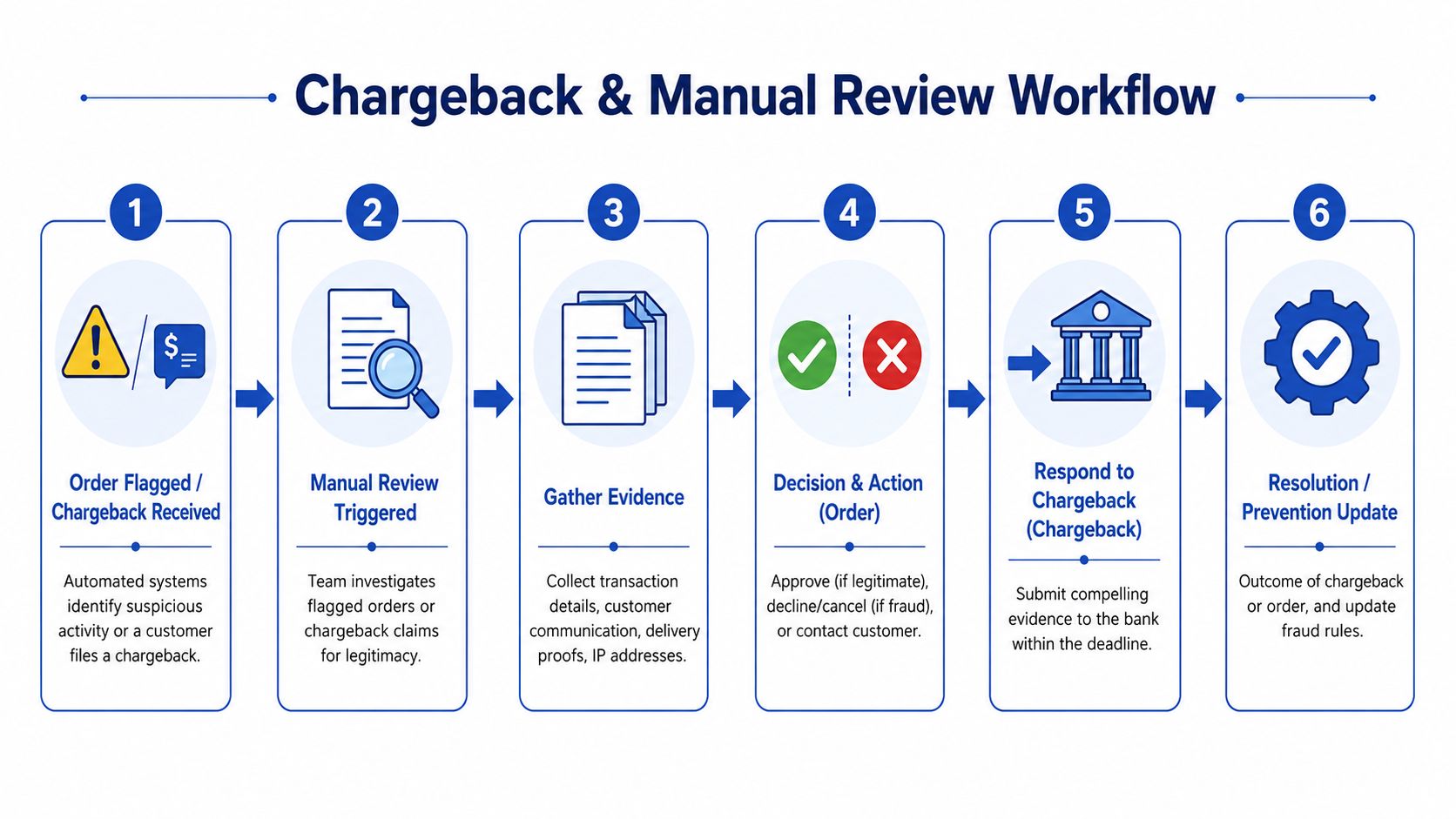

Managing Chargebacks and Manual Reviews

Even strong prevention won't stop every dispute. Some orders will be ambiguous at the point of purchase. Some chargebacks will arrive long after delivery. What matters is having a workflow your team can run consistently.

When to trigger a manual review

Manual review is expensive, so don't send everything there. Use it for orders that are valuable, unusual, or internally inconsistent.

Good triggers include:

- Data conflicts: Billing, shipping, email, and device signals don't line up cleanly.

- Order context: The basket is high risk for your category or difficult to recover once shipped.

- Customer history: The account is either brand new or behaving unlike its previous orders.

- Timing issues: Requests to change address, rush shipment, or split delivery appear after payment.

A reviewer should decide one of three things quickly: approve, cancel, or contact the customer for clarification.

What evidence actually helps

When a chargeback lands, merchants often scramble for proof they should have collected already. Build your evidence trail as part of normal operations.

Useful evidence usually includes:

- Order records: Item details, timestamp, payment authorisation, and checkout confirmation.

- Customer communications: Emails, support messages, and any post-purchase confirmations.

- Fulfilment proof: Carrier tracking, delivery confirmation, and address details used at dispatch.

- Account history: Prior legitimate purchases, account age, and changes to customer details.

Don't submit noise. Submit relevant evidence tied to the specific dispute reason.

A quick explainer can help teams visualise the process before they formalise it:

Fight or accept

Not every chargeback is worth contesting. If the order data is weak, the customer service trail is poor, or fulfilment records are incomplete, spending staff time on a weak response often costs more than it recovers.

Decision test: Challenge disputes where your evidence is coherent, complete, and easy for the bank to follow. Accept the rest, then fix the process gap that made the case weak.

The core value of chargeback handling isn't just recovery. It's feedback. Every dispute should tell you something about your checkout, fulfilment, communication, or fraud rules.

Balancing Security with Customer Experience

The biggest mistake new merchants make is assuming stricter always means better. It doesn't. A fraud system that rejects genuine customers is doing financial damage, just in a quieter way.

PwC UK notes that merchants must balance fraud prevention with the risk of false positives, and that UK-specific data on revenue lost to overly aggressive filters is still scarce in public guidance. That gap matters because teams can feel the pain in conversion without always proving it cleanly in a spreadsheet. PwC also notes that AI and machine learning are becoming essential for reducing false declines and improving this balance in practice, as outlined in PwC UK's fraud risk management perspective.

False declines are a commercial problem

A false decline doesn't just lose one order. It can lose the customer.

That's especially true for:

- First-time buyers: They haven't built trust with your brand yet.

- High-intent shoppers: They may switch to a competitor instead of retrying.

- Gift or seasonal purchases: Timing matters, so a delay can kill the sale altogether.

The customer often doesn't know why the order failed. They just experience friction and uncertainty.

What works better than blanket blocking

Merchants usually improve outcomes when they move from hard yes-or-no rules to a layered decision model.

A better approach includes:

- Risk scoring instead of automatic declines: Let several signals combine before you reject an order.

- Segment-aware policies: Returning customers shouldn't face the same treatment as unknown first orders in every case.

- Escalation paths: Use review or extra verification for grey-area orders rather than blanket rejection.

- Checkout clarity: If customers need to verify something, make the instruction obvious and low-friction.

If conversion is already under pressure, your checkout experience deserves the same scrutiny as your fraud stack. This guide to Shopify checkout optimization is useful for understanding where security friction and conversion friction often overlap.

Approving more good orders is just as important as stopping bad ones. That's the commercial heart of fraud prevention ecommerce.

How to judge whether your setup is too aggressive

You don't need perfect data to spot overcorrection. Look for these patterns:

- support tickets from confused buyers whose payment “should have worked”

- repeat customers unexpectedly routed into review

- heavy manual queues after promotions or launches

- fraud rules that no one wants to change because the logic is too tangled

When that happens, simplify. Remove duplicate rules. Re-test assumptions. Make sure each control has a clear job.

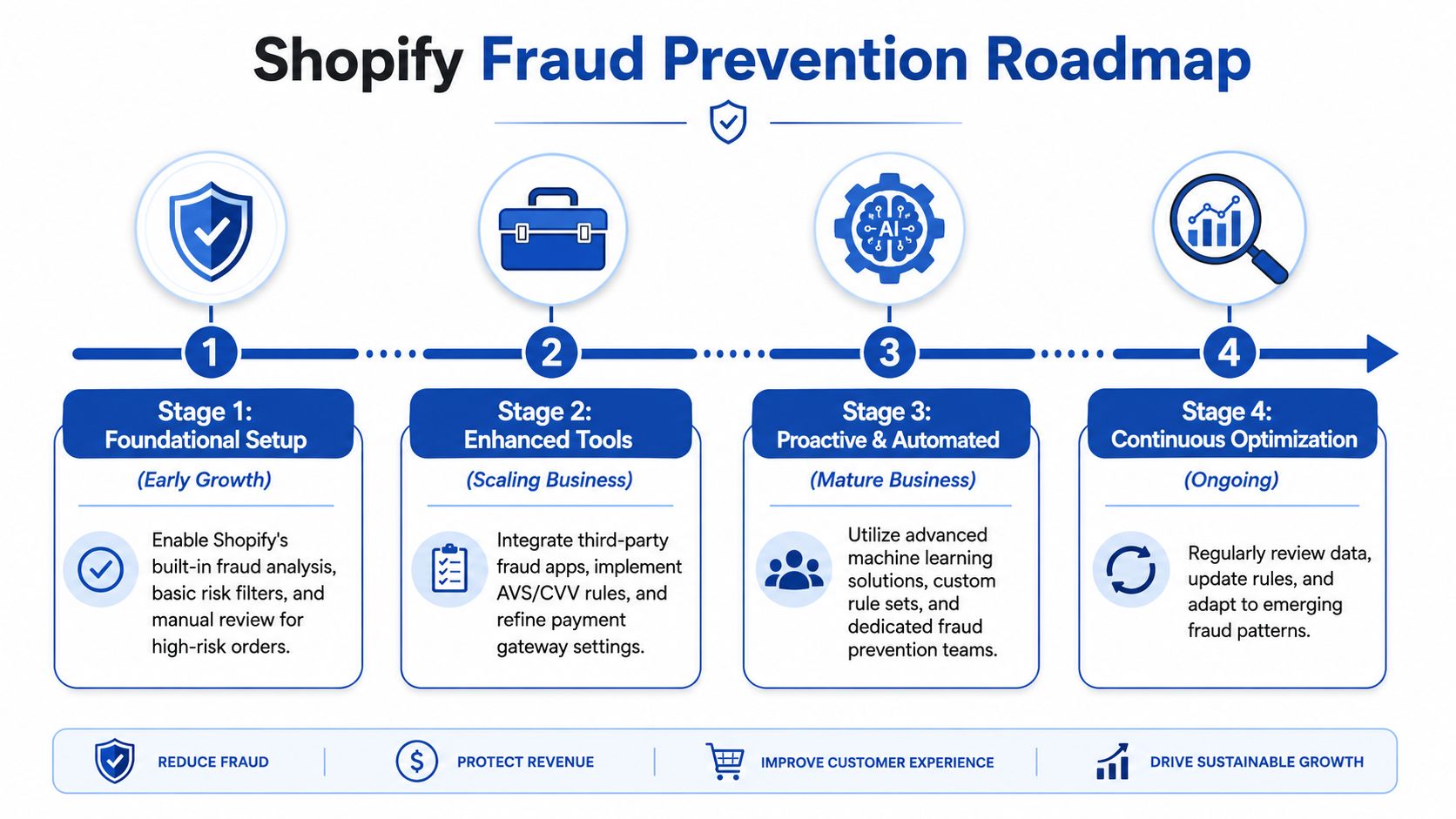

Building Your Fraud Prevention Roadmap on Shopify

Shopify gives merchants a useful starting point, but the right setup depends on scale, order complexity, and team maturity. The cleanest way to build is in stages.

Foundation

Start with native controls before adding software.

For most merchants, that means:

- Shopify's built-in fraud analysis

- payment gateway checks

- clear manual review rules for uncertain orders

- fulfilment controls so risky orders don't auto-ship

If you haven't reviewed gateway fit yet, this breakdown of top payment gateways for ecommerce in 2024 is a practical place to compare the operational side of payment choices.

Growth

As order volume rises, native tools stop being enough on their own. This is when merchants usually layer in specialist apps or external fraud platforms.

Look for tools that can support:

- richer risk scoring

- device and behaviour signals

- review queues with clear decision reasons

- better dispute evidence handling

- segmentation by market, product, or customer profile

Don't install multiple overlapping tools that all score the same order differently without a clear hierarchy. That creates confusion fast.

Scale

On Shopify Plus, a key advantage is workflow control. Shopify Flow can route tagged orders, pause risky fulfilment states, notify ops teams, or apply logic to specific order conditions. More advanced merchants also connect external fraud systems through APIs and feed outcomes back into internal processes.

At this stage, think beyond payment fraud alone. Security around integrations, apps, customer accounts, and business systems matters too. Teams reviewing broader platform risk may find this overview of Affordable Pentesting's SaaS security helpful when assessing third-party exposure.

Continuous optimisation

Fraud controls decay if no one maintains them. Product mix changes. Campaigns change. Fraud patterns change.

Keep a regular review cycle focused on:

- which orders were wrongly blocked

- which disputes you lost and why

- whether manual review criteria are still sensible

- whether fulfilment and support are collecting the right evidence

The roadmap isn't about building the biggest stack. It's about building one your team can operate.

Frequently Asked Questions about Ecommerce Fraud

Is SCA enough on its own

No. SCA is a strong UK payment safeguard, but it doesn't cover every abuse type. It helps against unauthorised payment fraud. It doesn't solve friendly fraud, account compromise after login, or operational issues that weaken chargeback defence.

What's the difference between AVS and CVV

AVS checks billing address details against issuer records. CVV checks that the buyer has the card security code during payment. They do different jobs and work best as combined signals rather than standalone verdicts.

Should every risky order go to manual review

No. Manual review should be reserved for orders where the value, uncertainty, or recoverability justifies staff time. If the queue gets too large, decisions slow down and fulfilment becomes messy.

Can automation replace a fraud analyst

Not fully. Automation is excellent at screening, scoring, and routing. Human review still matters for edge cases, policy judgement, and chargeback evidence quality.

What's the first thing a new Shopify Plus merchant should fix

Start with payment controls and fulfilment discipline. If risky orders can pass checkout and auto-ship before anyone checks them, the rest of the stack won't save you.

If you're scaling on Shopify and need help tightening checkout, payment flows, and operational logic without hurting conversion, Grumspot builds and optimises Shopify experiences that support growth properly. That includes the technical work behind cleaner checkouts, better integrations, and more reliable ecommerce operations.

Let's build something together

If you like what you saw, let's jump on a quick call and discuss your project

Related posts

Check out some similar posts.

- ecommerce development uk

Your complete guide to ecommerce development UK. Learn to plan, hire an agency, choose a tech stack ...

Read more

- pci compliance

Navigate PCI compliance requirements with our 2026 guide for UK merchants. Understand 12 rules, merc...

Read more

- woocommerce to shopify migration

Thinking about a WooCommerce to Shopify migration? Our guide covers data transfer, SEO, costs, and c...

Read more

- shopify design agency

Discover how a shopify design agency can transform your store with conversion-focused design, fast p...

Read more